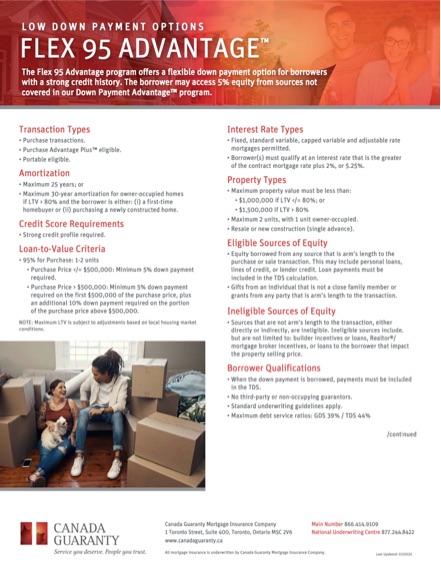

Flex 95 Advantage™ — Borrowed Down Payment Mortgages, Explained

A program by Canada Guaranty Mortgage Insurance Company that lets qualifying buyers use borrowed funds — like a personal loan or line of credit — for their down payment, instead of waiting years to save it.

Skip the Down Payment is our consumer-facing name for the Flex 95 Advantage™ program. It’s a real, regulated mortgage insurance product — not a workaround or a loophole. Canada Guaranty underwrites it; we’re the licensed brokers who place the deals with lenders. This page explains how it works in plain language.

What kinds of purchases qualify

The program is built around standard home purchases — your primary residence, or a duplex where you live in one of the units. It also works for new construction purchases through a single advance, and it can be paired with Canada Guaranty’s Purchase Advantage Plus™ for buyers including renovation costs in the mortgage. If you sell and move later, the insurance can be ported to your new home rather than being repurchased.

How long you have to pay it off

Standard amortization is 25 years. First-time home buyers and buyers of newly constructed homes can stretch to 30 years if the loan-to-value is above 80% — which most borrowed-down deals are. Longer amortization lowers monthly payments but costs more in interest over the life of the mortgage. Our specialists walk you through which option fits your situation.

What credit you need

A strong credit profile is required. Canada Guaranty doesn’t publish a hard minimum score, but the program is designed for borrowers who have demonstrated they can manage debt responsibly. If you’ve had recent credit issues, this isn’t the right program — but we have other options to discuss. Our calculator gives you a quick read on whether your credit story fits.

How much you can borrow

You can borrow up to 95% of the purchase price on a 1–2 unit owner-occupied home. The minimum down payment scales with the purchase price:

- Purchase price up to $500,000 — minimum 5% down

- Purchase price above $500,000 — minimum 5% on the first $500K, plus 10% on the portion above

So a $700,000 home would need: $25,000 (5% of the first $500K) + $20,000 (10% of the next $200K) = $45,000 minimum down. With Flex 95 Advantage™, those funds can be borrowed.

Note: Maximum LTV may be adjusted based on local housing market conditions in your area.

What kinds of properties qualify

The home you’re buying must be:

- A 1–2 unit residential property with at least one unit owner-occupied

- Resale or new construction (single advance)

- Below the program’s maximum property value cap: $1,500,000 if your LTV is above 80%, or $1,000,000 if your LTV is at or below 80%

If you’re looking at a property close to those caps, our specialists run the numbers to make sure you fit within the program before you make an offer.

Where your down payment can come from

This is the part that makes Flex 95 Advantage™ unique. Acceptable down-payment sources include:

- Personal loans from a bank, credit union, or other lender

- Lines of credit — personal or secured

- Lender credit — some lenders offer their own incentive funds toward your down payment

- Gifts from someone who is not a close family member

- Grants from any arm’s-length party (employer down-payment assistance programs, certain municipal grants)

The key phrase is “arm’s length” — the source has to be genuinely independent of the home sale itself. The loan or credit payments you’ll be making on those borrowed funds get factored into your debt service ratios (GDS and TDS).

What doesn’t qualify

Sources tied to the transaction itself are ineligible. The most common ones we see:

- Builder incentives or loans tied to a specific property purchase

- Realtor or mortgage broker incentives

- Any arrangement that artificially inflates or impacts the selling price

If a builder is offering you a “down payment match” or a realtor is offering cash-back at closing, those won’t count toward the Flex 95 Advantage™ minimum down payment — you’d need an arm’s-length source.

Other requirements

- Debt service ratios: GDS (gross debt service) maximum 39%, TDS (total debt service) maximum 44%. TDS includes your new mortgage payment, property taxes, heating, half your condo fees if applicable, AND the monthly payments on your borrowed down-payment funds.

- Qualifying rate: You must qualify at the higher of your contract mortgage rate plus 2%, or 5.25% — the federal stress test requirement that applies to all insured mortgages.

- No third-party or non-occupying guarantors. If you need a co-signer who isn’t living in the home, this program isn’t the right fit.

What it costs

All mortgage default insurance in Canada has a premium attached. For Flex 95 Advantage™, the premium falls within the industry-standard range for high-LTV mortgages and is added to your mortgage balance rather than paid upfront — so it gets amortized over the life of the loan. The premium is non-refundable.

If you have questions about how the premium affects your monthly payment, our specialists run those numbers for you alongside your pre-approval estimate.

What you’ll need to provide

Standard mortgage documentation applies — proof of income (pay stubs, T4s, NOAs), proof of the borrowed down-payment source (your loan or line-of-credit documents), credit consent, ID. Our team walks you through the full document checklist once you’re ready to move from estimate to application.

Canada Guaranty’s Flex 95 Advantage™ program sheet

For brokers, lenders, and buyers who want the official underwriting reference. This is the program sheet Canada Guaranty publishes for their Flex 95 Advantage™ product, last updated July 2025.

View official PDF →Flex 95 Advantage™, Down Payment Advantage™, Purchase Advantage Plus™, and Portable Advantage™ are trademarks of Canada Guaranty Mortgage Insurance Company.