Own a Home.

Skip the Down Payment.

Good credit and solid income? You may qualify to buy a home today — with zero down payment saved. Submit your details and a mortgage specialist will send your personalized pre-approval estimate within 5–10 minutes.

- BBB Accredited

- No credit pull to estimate

- Licensed Alberta brokers

- Powered by Canada Guaranty Flex 95™

Get Your Free Estimate

A specialist will review your numbers and email your estimate within 5–10 minutes.

We never pull your credit for this estimate. Your information is never shared or sold. For more information, please refer to our Privacy Policy.

What's your down payment situation?

Choose the option that best matches your situation.

We never pull your credit for this estimate. Your information is never shared or sold. For more information, please refer to our Privacy Policy.

When are you looking to buy?

This helps us tailor our follow-up to your timeline.

We never pull your credit for this estimate. Your information is never shared or sold. For more information, please refer to our Privacy Policy.

Your Income & Debts

Complete all fields and we'll calculate your result instantly.

Please complete all fields above.

We never pull your credit for this estimate. Your information is never shared or sold. For more information, please refer to our Privacy Policy.

Where should we send your results?

Your estimate will be calculated and sent shortly.

Please complete all fields above.

We DO NOT pull your credit. Your information is used only to reach out to you. No portion is shared with any third party. For more information, please refer to our Privacy Policy.

We'll be in touch shortly to discuss your options. Check your email for a copy of your results.

You're all set!

We've received your information and will be in touch shortly to discuss your pre-approval options.

The Skip the Down Payment program — and any mortgage with less than 20% down — requires solid credit history. Here's what good credit looks like and how to build it.

If you don't have any credit history yet, start with secured Visas from Scotia Bank and Home Trust — they're easier to approve for and a great first step. You can track your score for free at www.equifax.ca.

Down payment ranges and what credit you'll need

- 0–4% down: excellent credit, score above 680

- 5–9% down: score of 620+, no late payments or collections in the last 2 years

- 10–19% down: score of 580+, no recent late payments or collections

- 20%+ down: multiple lenders available depending on your interest rate tolerance

Tips to bump up your credit score

- If you've missed payments, try to open or maintain three credit accounts with perfect repayment going forward. (Student loans don't count.)

- Re-establishing payment history typically takes:

- ~12 months for one missed payment

- 2–3 years for 60- or 90-day late payments

- 3+ years for written-off debts (excluding minor collections like cell phone bills)

- Consumer proposals and orderly payment of debt are treated like a bankruptcy for mortgage purposes — wait times are significantly longer.

- Keep credit utilization low. Utilization is the ratio of balance to total credit limit. 30% or under is ideal.

- If you plan to purchase a home within 24 months, do not finance a vehicle purchase — the high utilization of that debt will reduce your score and your mortgage approval chances.

Why closing cards can hurt you

Say you have these accounts:

| Account | Limit | Balance |

|---|---|---|

| Credit Card A | $15,000 | $0 |

| Credit Card B | $10,000 | $0 |

| Credit Card C | $5,000 | $4,000 |

| Loan (orig. $20,000) | $20,000 | $17,000 |

Total utilization: $21,000 balance ÷ $50,000 total limit = 42% — that's healthy.

Now close Cards A and B (because you don't use them). New utilization: $21,000 ÷ $25,000 = 84% — that's bad. Your credit score could drop 50 points overnight.

A smarter path to homeownership

The federal government permits one type of no-down-payment mortgage — and we specialize in it. If you have the income and credit, you could be moving in sooner than you think.

Check Your Eligibility

Use our calculator to see if your credit and income qualify. No credit bureau pull — takes under a minute.

Get Pre-Approved

We submit your application to lenders who specialize in this program. One inquiry, done right.

Buy Your Home

Start shopping with confidence. The mortgage rate is the same as a 5% down payment — no penalty for skipping the savings wait.

Why choose Skip the Down Payment?

Everything you need to stop renting and start building equity — years sooner.

Stop Waiting, Start Owning

Average buyers wait 5–10 years to save a 5% down payment. With rising rents and home prices, this program changes that math entirely.

Same Rate as 5% Down

You won't be penalized on your mortgage rate simply because you didn't save a down payment. The rate is identical.

Build Equity Immediately

Every mortgage payment builds your net worth. We've helped hundreds of renters build tens of thousands in equity — years sooner.

No Broker Fees

As licensed mortgage brokers, the bank pays us — not you. Your only out-of-pocket costs are the lawyer (~$1,800) and optional inspection (~$500).

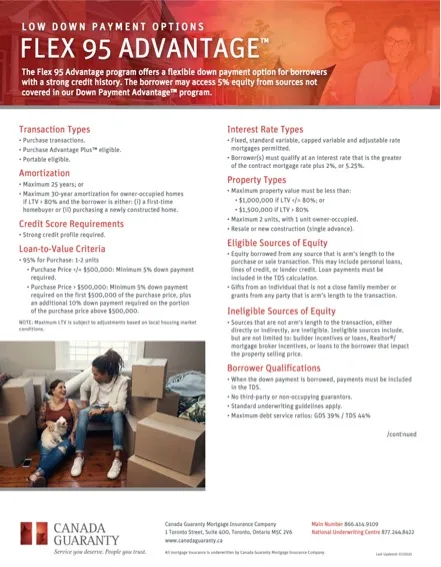

Behind Skip the Down Payment: the Flex 95 Advantage™ program.

A flexible down-payment program offered by Canada Guaranty Mortgage Insurance Company — we’re the licensed Alberta brokerage that places these files.

The Flex 95 Advantage™ program lets qualifying buyers use borrowed funds for their down payment instead of waiting years to save it. That borrowed money can come from a personal loan, a line of credit, or even a gift from someone outside your immediate family.

You can qualify with as little as 5% down on the first $500,000 of your purchase price (10% on any amount above that). Strong credit is required, and the down-payment loan payments factor into your debt service ratios — which is exactly what our calculator estimates for you up front.

As a licensed Alberta mortgage brokerage, we work directly with the lenders who place these files. Your numbers go to a specialist who validates them and submits the deal.

Program at a glance

- Up to 95% loan-to-value on homes up to $1.5M

- 25-year amortization standard (30 for first-time buyers)

- GDS 39% / TDS 44% maximum debt service ratios

- Industry-standard insurance premium added to mortgage balance

- Strong credit profile required

Flex 95 Advantage™ and Down Payment Advantage™ are trademarks of Canada Guaranty Mortgage Insurance Company.

Real Canadians. Real results.

Common questions

Quick answers to what most buyers ask before they get started.

Backed by lenders you trust

We work with major Canadian banks, credit unions, and monoline lenders to find the right fit for your situation.

Logos shown are property of their respective owners and represent lenders we work with. Final lender selection depends on your individual qualification.